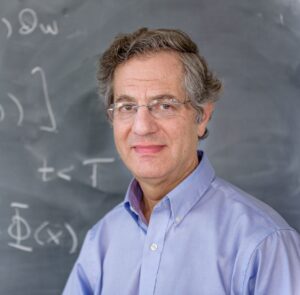

FARSHID M. ASL, PH.D

Instructor since 2005

LINKS:

Managing Director, Investment Management Division, Goldman Sachs, Farshid is currently the head of the Strategic and Quantitative Asset Allocation in the Investment Strategy Group, where he is responsible for the quantitative modeling and analysis of tactical views and strategic asset allocations. Previously, he spent two years as a strategist in the Fixed Income, Currency and Commodities and the Equity Divisions at Goldman Sachs, developing quantitative models for credit and volatility trading. Farshid joined Goldman Sachs in 2006 and was named managing director in 2011. Prior to joining Goldman Sachs, Farshid was a senior vice president of Risk Analytics at GMAC, where he focused on strategic direction and leadership in the development and operations of the risk management systems and processes for GM, GMAC and GM Asset Management. Farshid has been a program fellow and adjunct professor at Courant Institute of Mathematical Sciences at New York University since 2005. He has published various papers in quantitative journals and presented at conferences and has led a number of workshops in quantitative trading. Farshid earned a PhD in Stochastic Optimal Control and an MS in Financial Engineering from the University of Michigan in 2002. He is the recipient of the 2005 Carl T. Humphrey Memorial Alumni Award from Villanova University.